By Ryan Prete, Dec 13, 2023

In the shadow of the COVID-19 pandemic, geopolitical shifts, and economic fluctuations, mergers and acquisitions (M&A) landscape experienced a significant dip. Moving into 2024, the M&A scene, while still somewhat uncertain, shows the potential for a dynamic shift, reflective of the evolving global economic trends. In this article, we’ll review the key M&A activity trends from 2023 and examine the economic factors , geopolitical influences, and industry developments that could shape the M&A landscape in 2024.

Explore what could lie ahead for the IPO landscape in 2024

Table of Contents

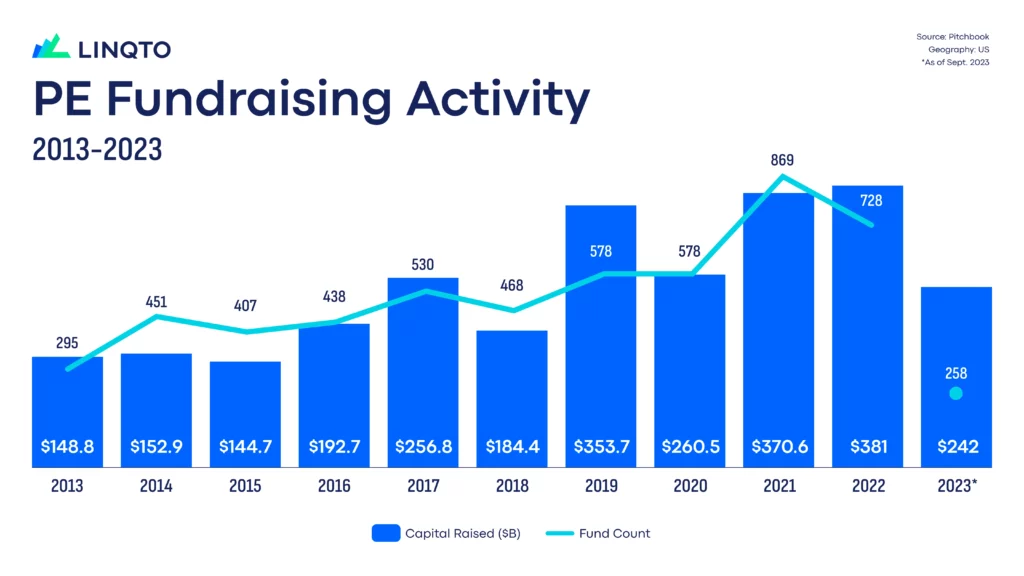

M&A activity witnessed a notable slowdown in 2023, coming off the back of unprecedented highs in 2021 and 2022. This year’s decline was influenced by a combination of rising interest rates, geopolitical tensions, and economic uncertainty, marking a shift from the previous years’ record-breaking activities. However, resilience was still evident in certain sectors, particularly technology and healthcare sectors, where strategic acquisitions were made, albeit more cautiously.

As of the publish date of this article, the global tally of completed M&A deals globally in 2023 stands over 23,000, with a total deal value exceeding $2 trillion , as reported by PitchBook. This figure is expected to rise to approximately 30,500 deals by year’s end, considering those already agreed upon, but not yet closed. For perspective, these numbers follow the staggering 41,345 deals in 2022 and a peak of 43,057 deals in 2021.

While2023’s figures may not rival the exceptional surge seen in the previous two years, they nonetheless reflect a robust M&A environment. The factors contributing to this year’s slower pace offer insights into the evolving dynamics of the global M&A market.

While2023’s M&A figures point to a resilient market, they couldn’t quite match the extraordinary surge witnessed in 2021 and early 2022. Several key factors contributed to this year’s deceleration in deal-making:

Rising Interest Rates: A significant driver of the 2023 slowdown was the increase of interest rates. This shift led to higher borrowing costs, prompting companies to reconsider the extent of debt they were willing to take on. The result was a more cautious acquisition strategy, impacting both the volume and value of deals made.

Reduced Leverage: Alongside rising interest rates, there was a noticeable trend toward reduced leverage. With the cost of debt financing climbing, businesses were more circumspect about relying heavily on borrowed funds for acquisitions. This shift translated into a more selective approach to M&A activities.

Regulatory Scrutiny: This year also saw heighted regulatory oversight, particularly in technology and healthcare sectors. This increased scrutiny added complexity to the deal-making process, making transactions more challenging and time-consuming to finalize.

Leverage the power of Startups! Make your move and accelerate your wealth journey creation today!

In a year of recalibrated strategies and selective deal-making, several standout M&A transactions emerged as reported by PitchBook. Here’s a snapshot of those deals that shaped the 2023 M&A landscape:

VMware and Broadcom: A milestone in the tech industry, Broadcom’s acquisition of VMware valued at approximately $69 billion. Announced in May and completed in November 2023, this deal birthed one of the largest and most diverse semiconductor and software entities in the world.

Activision Blizzard and Microsoft: Microsoft’s acquisition of Activision Blizzard, announced in January 2022 and finalized on October 18, 2023, for $68.7 billion, marked the largest deal in video game history to date.

Pioneer Natural Resources and ExxonMobil: In a significant move in the energy sector, ExxonMobil’s $59.5 billion all-stock deal for Pioneer Natural Resources was announced on October 11, 2023, at $253 per share.

Hess and Chevron: Another major energy sector transaction was Chevron’s acquisition of Hess Corporation for $53 billion, announced on October 23, 2023 and valued at $171 per share.

Seagen and Pfizer: Pfizer’s acquisition of Seagen, announced on March 30, 2023, for $43 billion, or $229 per share, was completed on August 22, 2023, marking a significant move in the pharmaceutical industry.

Looking towards 2024, while precise forecasts are challenging, some industry experts anticipate a resurgence in M&A activity, underpinned by several factors:

Easing Economic Uncertainty: Improvement in economic conditions and a return of investor confidence could create a more conducive environment for M&A. Companies might pursue acquisitions more aggressively to enhance their market reach, access to new technologies, and achieve strategic objectives.

Strategic Consolidation: The ongoing need for businesses to adapt and grow in the face of changing market conditions and technological advancements could drive a wave of strategic consolidations. This trend is expected to be particularly pronounced in sectors where scale and efficiency are key competitive advantages.

Technological Innovation: The rapid pace of technological progress is likely to be a major catalyst for M&A activity in 2024. Companies, especially those lacking in certain technological capabilities, might seek acquisitions to integrate advanced technologies like artificial intelligence, cloud computing, and cybersecurity into their operations, maintaining a competitive edge. This pursuit of technological advancement through M&A is expected to fuel deal activity across various industries, particularly in technology-driven sectors.

Discover key trends and investment strategies in our 2024 market forecast blog.

Analysts believe that several factors could contribute to a surge in M&A activity in the fintech sector in 2024. A primary driver is expected to be the consolidation among smaller players seeking to expand their scale and reach. Well-established fintech companies are likely to target startups that bring innovative technologies or specialized expertise to the table.

Furthermore, efforts towards geographical expansion are anticipated to spur cross-border M&A deals. This expansion isn’t about increasing market footprint; it’s about tapping into new and emerging markets, bringing innovative fintech solutions to a broader audience.

Strategic partnerships are also set to play an important role. Collaborations between fintech firms and traditional financial institutions may lead to a variety of joint ventures, acquisitions, or other forms of collaboration. These alliances could bridge the gap between traditional banking and modern fintech, creating synergies that benefit both sectors. Additionally, the evolving landscape of regulatory compliance is expected to be a significant catalyst for M&A activity. Firms specializing in compliance solutions may find themselves at the center of M&A discussions as companies seek to navigate the increasingly complex regulatory environment effectively.

The AI sector is also primed for an upsurge in M&A activity in 2024, fueled by several drivers. Companies aiming to acquire AI capabilities and expertise to enhance their products and services will drive consolidation. Startups with innovative AI solutions could be acquired by established companies seeking to stay ahead of the curve. The drive for technological advancement and talent acquisition in AI will also play a significant role in stimulating M&A activity.

Analysts believe the healthcare sector could see a surge in M&A deals for a number of reasons. Driven by factors such as the aging population, rising prevalence of chronic diseases, the transition to value-based care, and the convergence between pharmaceuticals and biotech sectors. Additionally, a growing focus on consumer-centric healthcare solutions and the complex regulatory environment are generating a demand for specialized expertise and innovative healthcare solutions. These dynamics are expected to encourage healthcare companies to pursue acquisitions actively.

A significant increase in M&A activities is projected for 2024. Factors driving this include the consolidation of smaller entities looking to scale, and the deeper integration of digital assets into mainstream finance, potentially leading to strategic partnerships and acquisitions. The sector is also likely to benefit from clearer regulatory frameworks and increasing institutional adoption, creating a conducive environment for M&A activities. Furthermore, technological advancements within the digital asset space are expected to attract acquisitions, particularly of startups offering innovative technologies.

Step into the high-reward world of private equities. Don’t wait, your portfolio expansion starts here!

Private market investors, while not directly involved in private equity deals, they can still strategically benefit from an uptick in M&A activity in the private market through various approaches:

Staying Informed: Regularly monitoring industry trends, regulatory developments, and potential M&A activity in the private market can help investors identify promising investment opportunities and make more educated decisions regarding their private market investments. Regular engagement with insightful resources like Linqto’s blog, which provides updates on market trends is beneficial.

Each of these strategies requires careful consideration and due diligence, aligning with individual investment goals and risk tolerance.

Despite not reaching unprecedented levels of 2021 and 2022, M&A activity held steady in 2023, indicating a resilient market. Looking ahead to 2024, there is a general anticipation of increased M&A activity, supported by a blend of factors conducive to deal-making. These include an improving economic landscape, ongoing technological advancements, shifting regulatory landscapes, and strategic business objectives.

Key sectors like artificial intelligence, healthcare, fintech, and digital assets, having drawn considerable interest from institutional investors recently, are expected to experience a notable increase in M&A activity. The coming year promises to offer valuable insights into how these drivers will shape the M&A environment, potentially influencing the frequency and scale of transactions across various industries.

While forecasting the exact trajectory of the M&A market remains challenging, staying abreast of market trends is important for investors. Regularly engaging with resources such as Linqto’s blog can provide valuable insights into the evolving M&A landscape, helping investors to navigate the market more effectively.

This material, provided by Linqto, is for informational purposes only and is not intended as investment advice or any form of professional guidance. Before making any investment decision, especially in the dynamic field of private markets, it is recommended that you seek advice from professional advisors. The information contained herein does not imply endorsement of any third parties or investment opportunities mentioned. Our market views and investment insights are subject to change and may not always reflect the most current developments. No assumption should be made regarding the profitability of any securities, sectors, or markets discussed. Past performance is not indicative of future results, and investing in private markets involves unique risks, including the potential for loss. Historical and hypothetical performance figures are provided to illustrate possible market behaviors and should not be relied upon as predictions of future performance.

Ryan is a financial writer for Linqto, known for his original blog content, articles, and other works. He previously worked as a financial writer at PitchBook Data, where he covered private equity, and as a reporter for Bloomberg in Washington D.C.,where he reported on tax policy. Ryan has also reported on cybersecurity policy for Inside Washington Publishers. His work has been featured in The Wall Street Journal, Axios, Yahoo News, and Reuters. He is a graduate of the University of California, Santa Barbara.